L’automobile a les ventes en poupe

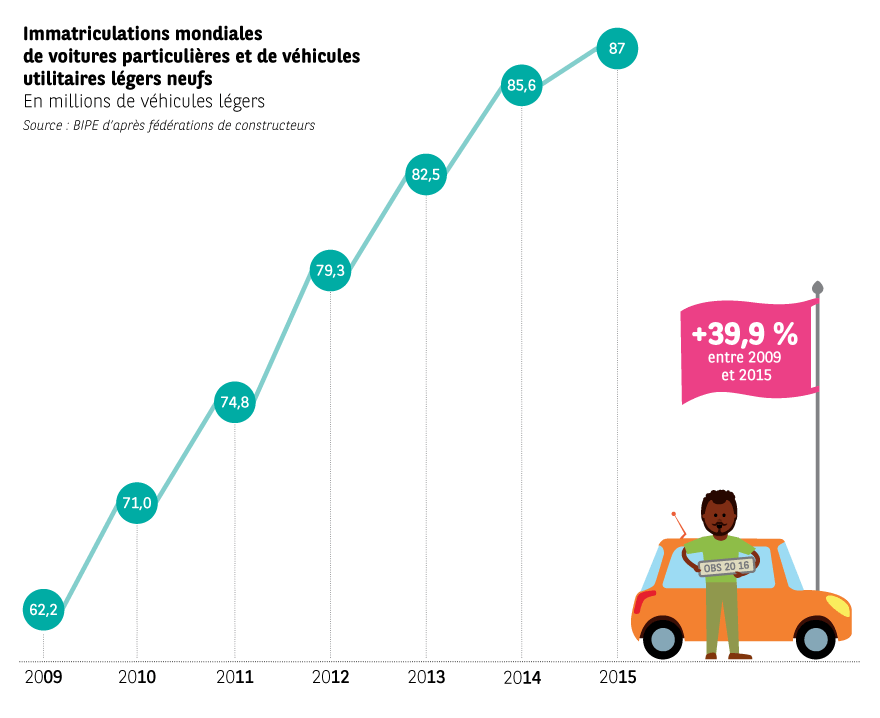

Nouveau record : 87 millions d’immatriculations neuves de véhicules légers. Cette excellente santé se traduit aussi au plan financier. La plupart des constructeurs automobiles ont connu des résultats en hausse, voire en forte hausse. Ce total de ventes exceptionnel masque cependant des disparités d’une zone à l’autre, en phase avec les conjonctures économiques.

Une Amérique record

En deux années, la baisse marquée des prix du pétrole, des taux d’intérêt extrêmement bas et la confiance retrouvée dans l’économie ont permis au marché américain de retrouver son faste d’antan. Les ménages sont restés demandeurs alors que les entreprises rajeunissaient leur parc après des années d’économies. 2015 a été synonyme d’un millésime exceptionnel pour l’industrie automobile américaine qui a battu le record de ventes de 2000 avec 17,4 millions d’unités écoulées (pick-up inclus, +5,7 %). Cette appétence pour le neuf s’est matérialisée par une normalisation du ratio entre occasion et neuf passé de 3,2 en 2010 à 2,2 en 2015. Les voisins mexicains ont également profité de la dynamique avec des ventes en hausse de 19 % pour 1,4 million de ventes.

Une Europe unie à la hausse

Même euphorie en Europe. Après des années de déprime suite à la crise de 2008-2009, durant lesquelles le parc a vieilli, on a assisté à la poursuite d’un phénomène de rattrapage mécanique. Regain de pouvoir d’achat pour les ménages, amélioration sur le front de l’emploi et des revenus, baisse des prix des carburants et inflation générale quasi nulle ont composé la martingale qui explique la reprise des marchés. Les ratios occasion sur neuf qui avaient plafonné au moment de la crise tendent à se normaliser. Séduits par les nouveautés, les ménages ont commencé à regagner le chemin des concessions, dans l’optique de renouveler pour partie les véhicules achetés en masse au moment des primes à la casse en 2009-2010. Les entreprises profitent, quant à elles, d’un cycle d’investissement favorable et d’offres de location en longue durée séduisantes pour renouveler leurs flottes.

Les marchés italien et espagnol qui avaient perdu jusqu’aux deux tiers de leur substance ont ainsi bondi l’an passé (respectivement +16 % en Italie et +23 %). En Espagne, le seuil du million de véhicules particuliers a de nouveau été atteint pour la première fois depuis 2008. Avec des reprises enclenchées plus tôt, les marchés allemand, français et britannique enregistrent des croissances moins marquées, mais néanmoins très positives, comprises entre 5 et 7 %.

Un moteur des ventes chinoises qui hoquette

En Chine, le ralentissement macroéconomique a entraîné, comme en 2014, une nouvelle réduction du taux de croissance des ventes. Après dix dernières années d’une expansion fulgurante, le premier marché mondial (27 % du total en 2015) a bouclé l’année en progression de moins de 6 %, pour 23,7 millions de véhicules. En début d’année, la dynamique des ventes était atone, subissant les contre-coups d’achats d’anticipation panique, suite à des rumeurs fin 2014 de restriction des droits à l’immatriculation dans certaines villes. Pire, pour la première fois depuis le décollage du début du millénaire, des glissements annuels négatifs ont été enregistrés durant les mois d’été.

Le ralentissement de la croissance économique et les chocs boursiers ont précipité une crise de confiance qui a refroidi les candidats à l’achat.

Il aura fallu une mesure publique de réduction des taxes sur les véhicules de petites cylindrées pour voir le marché repartir de l’avant lors des derniers mois de 2015.

Le Japon toujours en décroissance

Au début des années 1990, le marché japonais s’établissait à plus de 7 millions de véhicules légers. Depuis une dizaine d’années, il oscille entre 4 et 5 millions d’unités, au gré des mesures de soutien publiques. La troisième économie mondiale a évité de peu un deuxième épisode de récession mi-2015. La hausse de TVA intervenue en avril 2014 (de 5 % à 8 %) freine également la consommation de biens durables, notamment d’automobiles.

En prévision de cette mesure, les ménages avaient anticipé leurs achats. Ils désertent les concessions depuis son entrée en vigueur. Les mini-voitures de moins de 660 cm3, spécificité japonaise, ont par ailleurs vu leurs niveaux de taxes annuelles augmenter en avril 2015. Cette même année, leurs ventes ont décroché de 16,6 % tandis que les véhicules traditionnels perdaient 4 %. Au total, le marché nippon a perdu plus de 10 % en 2015.

Le Brésil à la peine

Entré en récession en 2015, le Brésil doit faire face à des conditions économiques difficiles, notamment une forte augmentation du taux de chômage conjuguée à une faible disponibilité du crédit. La crise politique entachée par des scandales de corruption n’a fait que dégrader une situation déjà extrêmement tendue. Dans ce contexte, la baisse du marché brésilien enregistrée en 2015 est la plus forte depuis 28 ans. Les ventes de voitures et de véhicules utilitaires légers ont en effet diminué de 25,6 % à 2,48 millions d’unités.