Des offres segmentées qui séduisent

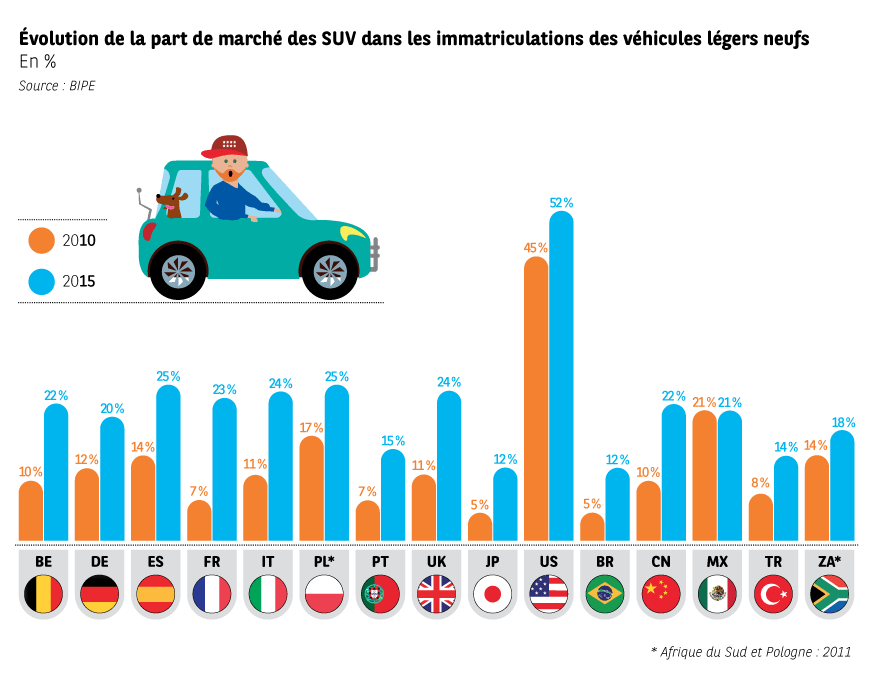

Les SUV prennent de la hauteur

Premier segment à tirer son épingle du jeu, celui des SUV. Représentant plus de 50 % (pick-up inclus) des immatriculations de véhicules légers aux États-Unis, la part de marché des SUV en Europe est passée de 8 % en 2010 à 20 % en 2015. Leur succès est particulièrement marquant en Italie (22 %), en Espagne (21 %) et au Royaume-Uni (20 %). Même au Japon où la croissance des ventes reste pourtant limitée, les automobilistes, plus particulièrement les jeunes générations, sont conquis par ces modèles. Les pays émergents ne sont pas en reste, les SUV représentant désormais près d’un quart des ventes en Chine.

Adaptés à la circulation urbaine et répondant dans la plupart des cas aux exigences environnementales, les SUV attirent à la fois pour leur côté pratique et rassurant, leurs lignes ludiques. Dans certains pays comme la Chine, le statut social qu’ils véhiculent est plébiscité. Un succès logique quand on sait que 70 % des automobilistes des pays émergents, et jusqu’à 82 % en Chine, estiment que l’image renvoyée par la voiture en termes de niveau de vie, de statut social est importante, contre « seulement » 52 % en moyenne 15 pays.

C’est en fait l’ensemble des marques qui a su se saisir de cet engouement du consommateur, voire l’anticiper. Nissan Qashqai, initiateur de la vague en Europe, Renault Kadjar, Volkswagen Tiguan 7 places, Peugeot 3008, Audi Q2, le Mercedes GLC coupé, les offres sont multiples… En Chine, Haval, la marque du constructeur chinois Greatwall entièrement dédiée aux SUV, fait un tabac. De nouveaux acteurs comme Seat, Skoda, Subaru et même Jaguar ou Maserati feront prochainement leur première incursion sur le segment.

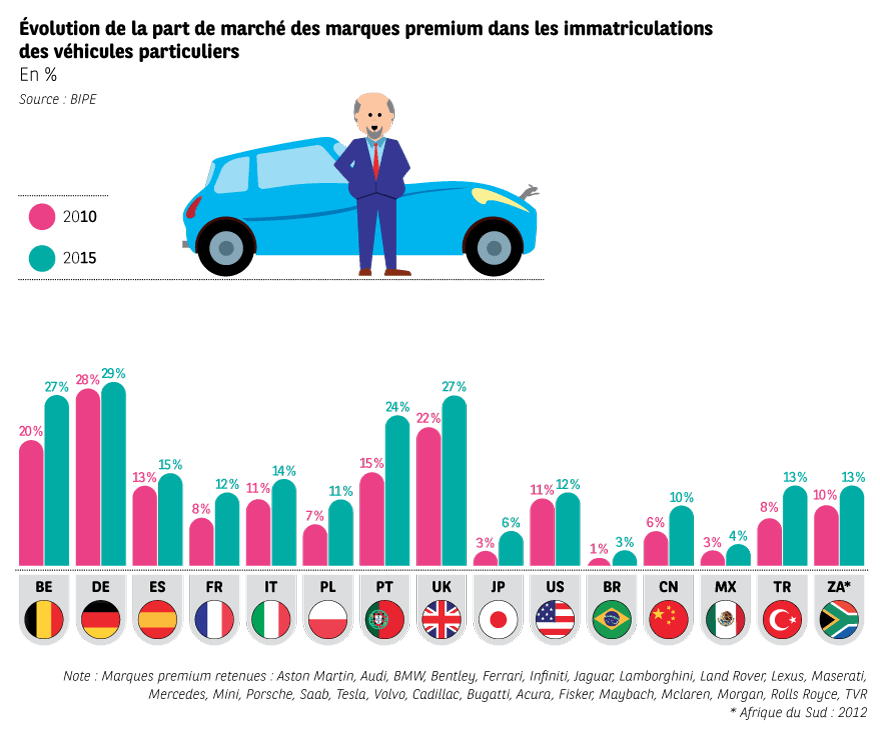

Nouveaux acheteurs pour marques premium

Autre illustration du ré-enchantement du marché automobile, l’intérêt croissant des automobilistes pour les marques premium. Entre 2010 et 2015, leurs ventes ont progressé de manière significative.

En Chine, leur part de marché a presque doublé, passant de 6 % en 2010 à 10 % en 2015. Jusqu’alors cantonnées aux segments des grandes berlines traditionnelles, les marques premium investissent aujourd’hui des segments plus compacts, particulièrement prisés par les jeunes femmes de classe aisée. L’arrivée sur le marché de la génération des second-time buyers (la première cohorte de renouvelants après le décollage du marché il y a 10 ans), explique aussi cette poussée du premium, le renouvellement étant fréquemment synonyme de montée en gamme. Et les mesures de restriction à l’achat dans les grandes villes privilégient mécaniquement les acheteurs potentiels aux revenus les plus élevées, plus susceptibles d’opter pour les marques premium.

En Europe, le marché du haut-de-gamme neuf reste essentiellement porté par les entreprises. Les solutions de financement comme la location longue durée permettent en effet de proposer des loyers compétitifs, le lissage dans le temps du coût d’entrée à l’achat, et garantissent le zéro souci (entretien et maintenance compris dans le loyer). L’achat de ce type de véhicules permet aussi de conserver une valeur résiduelle relativement élevée. Avec la diffusion de ces solutions de financement auprès des ménages, tout porte à croire que les Européens concrétiseront plus aisément leur rêve. Ils sont déjà 53 % à regarder les véhicules haut de gamme avec envie.

Aux États-Unis, où certaines marques non commercialisées en Europe sont présentes (Cadillac, Lincoln, Acura…), le marché du premium reste dominé par les spécialistes allemands BMW et Mercedes. La part de marché du haut-de-gamme s’établit à 14 % des ventes, une part stable sur les cinq dernières années.

Au Japon, à contre-courant de l’évolution du marché global, la part des marques haut-de-gamme a progressé dans les ventes entre 2010 et 2015.

En Afrique du Sud, où BMW et Mercedes détiennent des usines, les marques premium sont également plébiscitées (13 % des ventes en 2015).

Le futur en état de marche

Au cœur de ce que l’on pourrait appeler une « technofolie » imposée par le contexte économique, sociétal, environnemental et scientifique, l’automobile se présente comme un catalyseur d’innovations. Elle attire de nouveaux acteurs industriels et technologiques. Elle séduit de nouveaux profils de clientèles à qui l’automobile traditionnelle n’aurait pas suffi. Consacré l’an dernier à la voiture autonome et aux nouvelles technologies automobiles, L’Observatoire Cetelem de l’Automobile 2016 mettait en évidence qu’un automobiliste sur trois se déplacerait plus souvent si le véhicule était connecté.

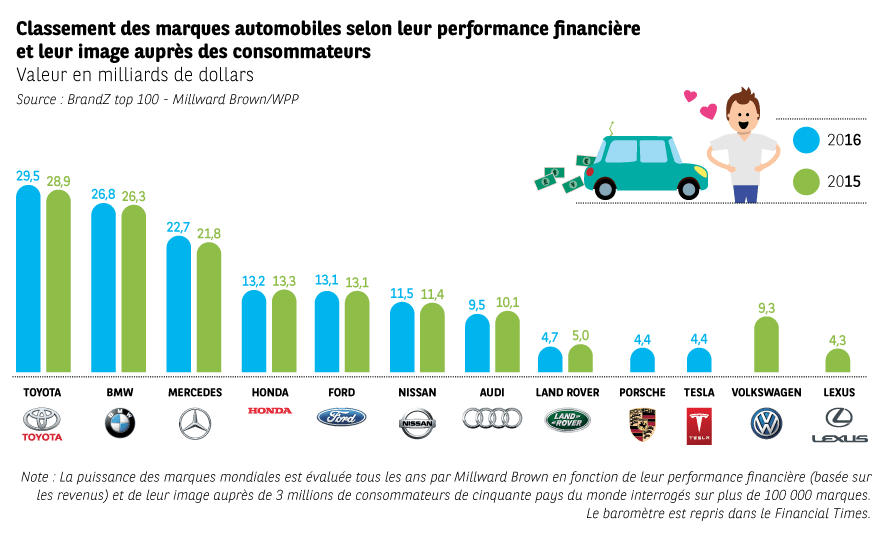

Un nouvel entrant fait beaucoup parler de lui. Premier constructeur automobile à entrer en bourse outre-Atlantique depuis les années 50, Tesla est née dans la Silicon Valley et s’est spécialisée dans la commercialisation de véhicules électriques haut-de-gamme. Elle a pour ambition d’égaler la capitalisation boursière d’Apple à horizon 2025. Sa popularité grandissante de 2012 à 2015 est indéniable, partout dans le monde. Ainsi, Tesla aurait enregistré plus de 300 000 réservations pour son prochain Model 3. Et pour la première fois en 2016, signe que « le futur, c’est maintenant », la marque figure dans le top 10 des marques automobiles les mieux valorisées du baromètre BrandZ Millward Brown.

Paroles de consommateurs

« La voiture connectée comme la Tesla, que j’ai essayée récemment, me fait vraiment envie. On parle d’une voiture qui est plus qu’un véhicule, la connexion permet de faire ce qu’on ferait avec un ordi dans sa voiture. Pour les geeks, c’est génial, on est comme chez soi ! »