Épargne ou dépenses ?

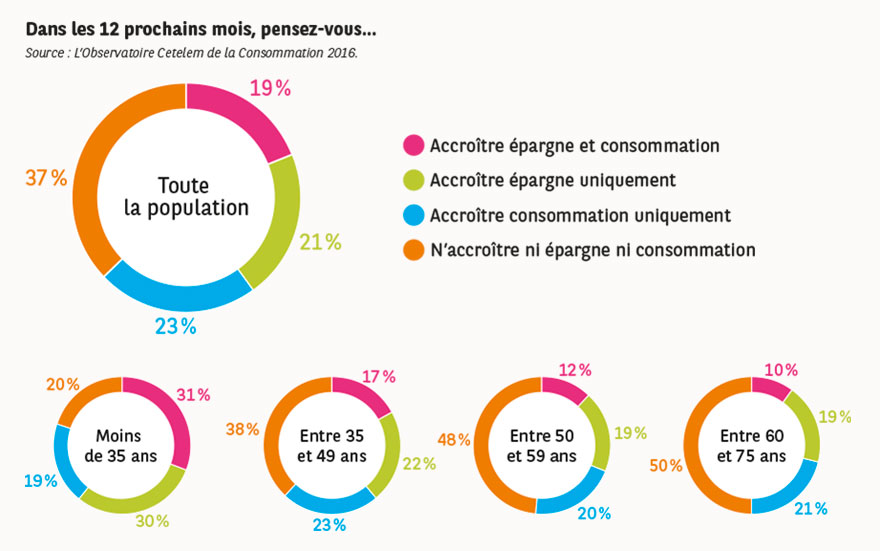

Des « cigales » et des « fourmis » à parts égales

42 % des Européens déclarent qu’ils vont davantage épargner au cours des douze prochains mois (+7 points vs l’Observatoire Cetelem 2015), mais seuls 9 % le feront de façon certaine. À l’inverse, 39 % vont plutôt s’autoriser davantage de dépenses (+4 points vs l’Observatoire Cetelem 2015). Mais là encore, ils sont très peu à être certains de le faire (6 %).

Du côté des fourmis, promptes à épargner, on trouve les Italiens, les Danois, les Britanniques et les Portugais. Du côté des cigales portées sur davantage de consommation, les Polonais, les Tchèques et les Slovaques sont surreprésentés. Il est à noter que 19 % des Européens déclarent qu’ils vont à la fois augmenter leur épargne et leurs dépenses.

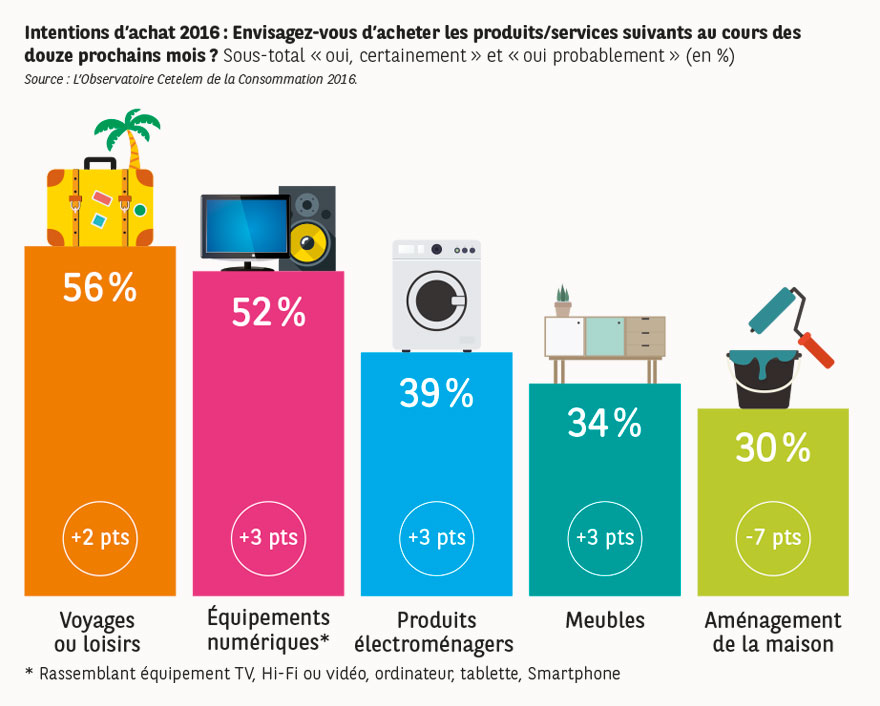

Voyages et loisirs toujours en tête

Avec 56 % des intentions moyennes, ces postes sont en hausse notamment en Espagne, en Italie et au Royaume-Uni. L’Allemagne et surtout la France, à cause des attentats, font bande à part. Les Français devraient se reporter sur d’autres achats, notamment l’automobile et les équipements numériques.

Le grand perdant semble être l’habitat. Alors que les intentions d’achat en bien immobilier sont stables (10 %), les travaux d’aménagement-rénovation, historiquement le troisième poste d’achat (30 %) ont très nettement chuté (-7 points) notamment en Italie, en Pologne et au Royaume-Uni. Les meubles figurent en quatrième position en augmentation de 3 points. Les équipements numériques sont massivement plébiscités : smartphone 32 %, hi-fi vidéo 26 %, tablette 21 % et micro-ordinateur 21 %, tous en nette hausse hormis les tablettes.