Connexions en cours

Il y a prix et prix !

En attendant les véhicules 100 % autonomes, les automobilistes ont de nombreuses attentes en matière de véhicules connectés. Et le consommateur, souvent opposé à toute augmentation tarifaire, accepte cette fois-ci un renchérissement du prix de l’automobile. Il estime que les fonctionnalités offertes par la voiture connectée lui sont véritablement utiles et justifient un surcoût. Loin d’être un gadget, la voiture connectée se présente bel et bien comme un levier de croissance pour les marchés automobiles !

Les aides à la navigation : indispensables !

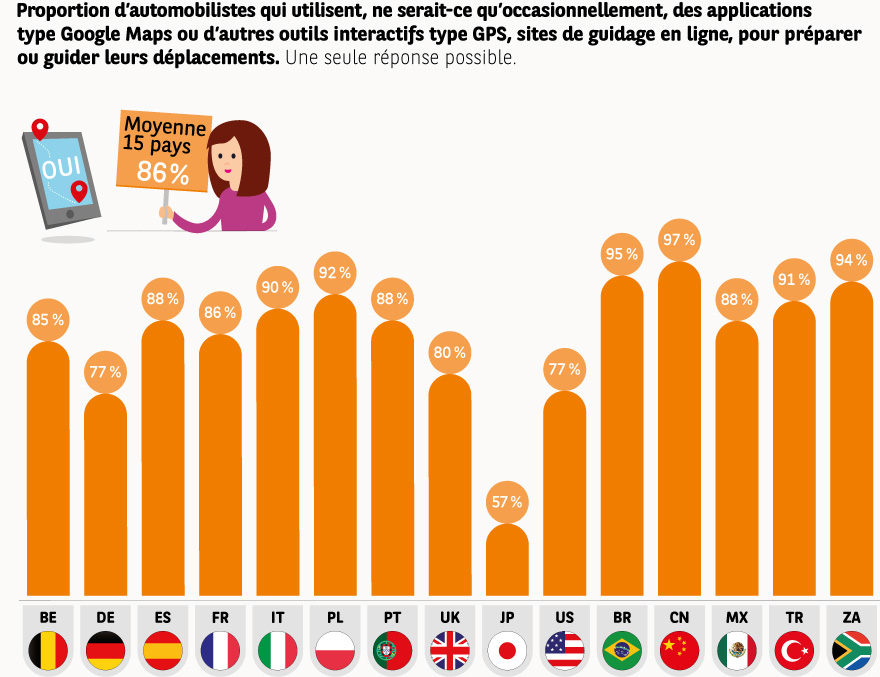

Les outils d’aide à la navigation sont considérés comme précieux pour les automobilistes interrogés par l’Observatoire Cetelem : 86 % d’entre eux déclarent s’en servir pour préparer ou guider leurs déplacements.

Pour les consommateurs des pays émergents, ces outils sont même devenus incontournables pour la navigation : 97 % des Chinois et 95 % des Brésiliens déclarent s’en servir.

En revanche, les Japonais semblent moins adeptes de ces outils et ne les citent qu’à 57 %.

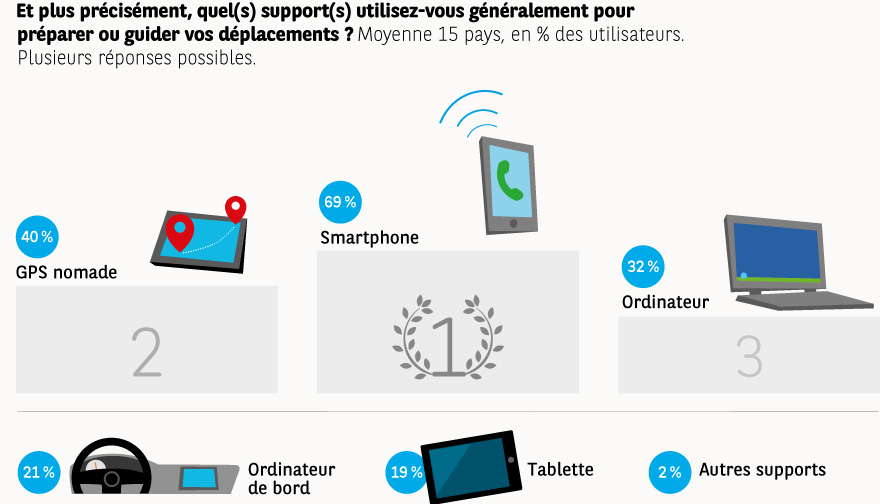

Naviguer, c’est d’abord consulter son smartphone

L’application Google Maps, que l’on peut installer gratuitement sur la plupart des smartphones, figure parmi les applications mobiles les plus utilisées au monde. Il n’est donc pas surprenant que 69 % des automobilistes mondiaux interrogés privilégient le smartphone pour préparer ou guider leurs déplacements, devant le GPS nomade (40 %) et l’ordinateur (32 %). Aux États-Unis, ils sont même 88 % à être habitués à naviguer grâce au smartphone.

Bien qu’étant placé au 4e rang, la performance de l’ordinateur de bord intégré au véhicule est notable.

Les Japonais, qui n’ont adopté les smartphones que récemment, sont les plus nombreux à déclarer utiliser les systèmes intégrés au tableau de bord pour leur navigation (36 % vs 21 % en moyenne 15 pays). Par ailleurs, ce sont les Turcs, qui consultent le plus leur tablette (30 % vs 19 % en moyenne).

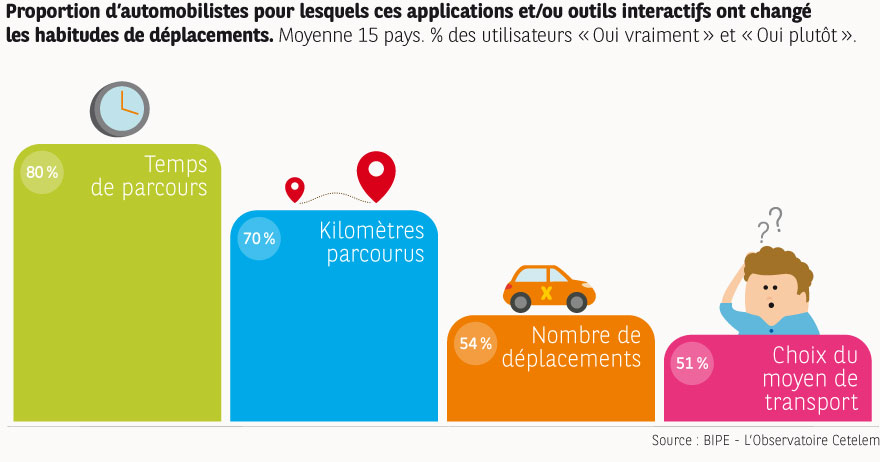

Des outils pour gagner la course contre la montre

Les applications de navigation, disponibles dans le véhicule et/ou via le smartphone ou Internet en général, impactent fortement la mobilité des individus.

Dans les pays émergents, l’optimisation du temps de parcours est constamment recherchée : pour 95 % des Brésiliens et 94 % des Chinois, les outils de navigation ont permis de gagner du temps. En Europe, les Polonais sont très nombreux à affirmer (88 %) que leurs temps de parcours sont positivement impactés par ces outils.

Les applications d’information en temps réel pour guider les déplacements et les choix de modes de transport sont nombreuses en Chine. Au Brésil, 70 % déclarent optimiser leurs choix de moyens de transport grâce aux applications. À l’inverse, aux États-Unis, seulement 29 % des automobilistes déclarent que les outils de navigation ont une influence sur leur choix de moyen de transport.

Voiture connectée, attention au prix !

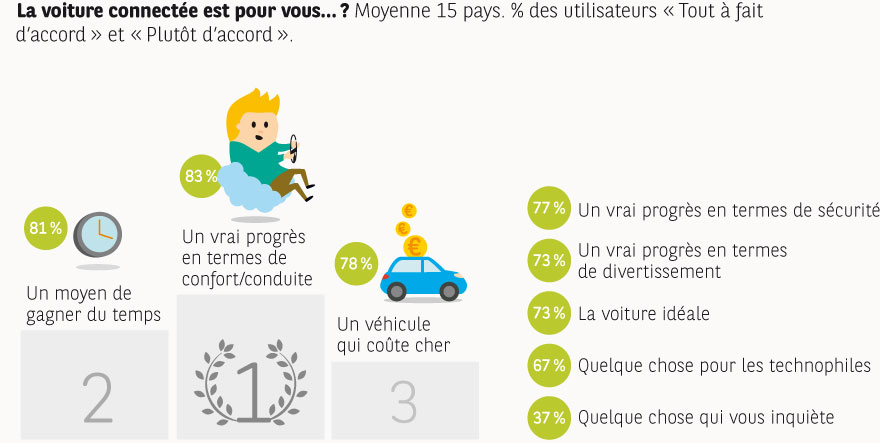

La voiture connectée est associée à des notions très positives par la majorité des automobilistes interrogés.

Pour 83 % d’entre eux en moyenne, elle est synonyme de véritable progrès en termes de confort de conduite, pour 81 % de gain de temps et pour 77 % de progrès de termes de sécurité. Toutefois, 78 % considèrent que la voiture connectée rime avec cherté.

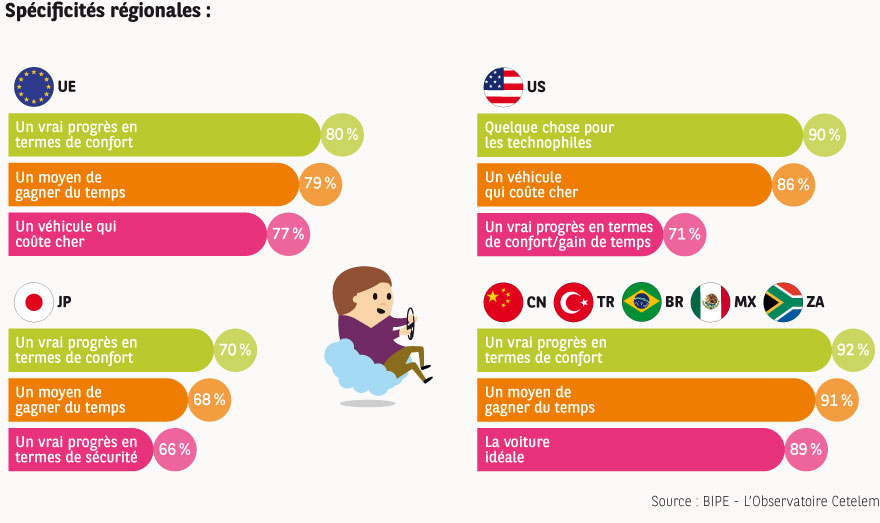

Les automobilistes des pays émergents se montrent les plus enthousiastes vis-à-vis de la voiture connectée, estimant qu’elle représente un réel progrès en termes de confort de conduite.

Au Japon, les consommateurs n’identifient dans leur top 3 que des bénéfices pour la voiture connectée : confort, gain de temps et sécurité y sont particulièrement valorisés.

Les inquiétudes et réticences vis-à-vis de la voiture connectée se situent plutôt du côté des autres pays occidentaux. Les Européens savent que cela aura un coût. Les Américains considèrent à 90 % que la voiture connectée est réservée aux technophiles : un comble pour le pays où circule déjà la Google Car dans certains états (Californie, Texas) !

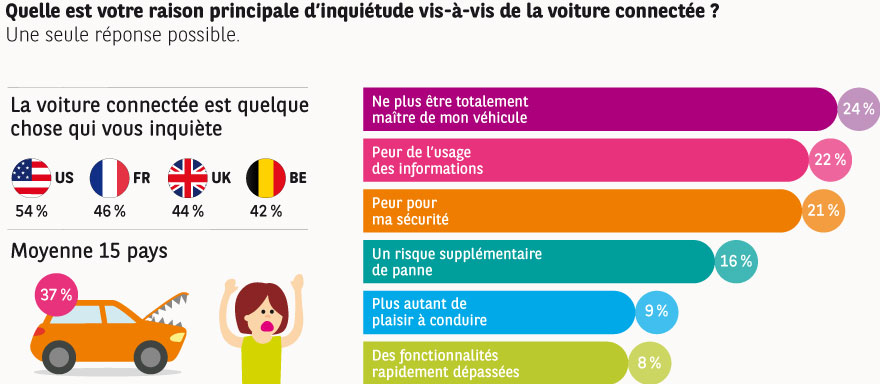

Si la voiture connectée représente avant tout une avancée majeure pour les automobilistes, dans certains cas – peu nombreux- elle suscite aussi des craintes : 37 % avouent que la voiture moyenne). connectée les inquiète, ils sont 54 % aux États-Unis et 46 % en France. Les Allemands, quant à eux, déclarent redouter le plus l’usage des informations communiquées par la voiture et l’éventuelle perte de contrôle sur les données privées. Les Italiens, amoureux de l’automobile, sont plus nombreux à craindre de devoir renoncer au plaisir de conduire (17 % vs 9 % en moyenne).

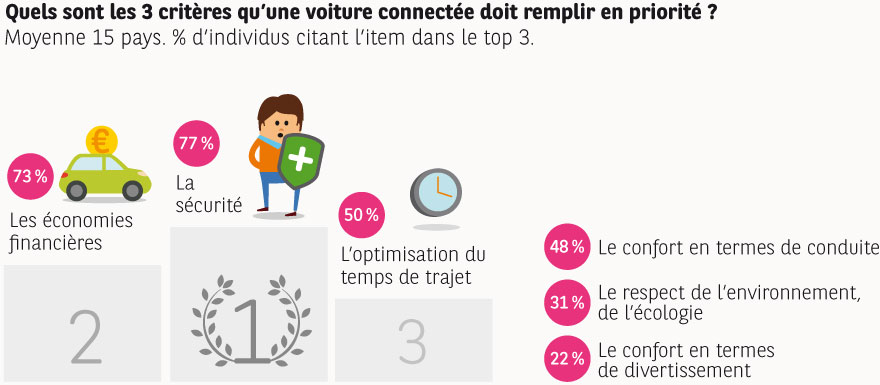

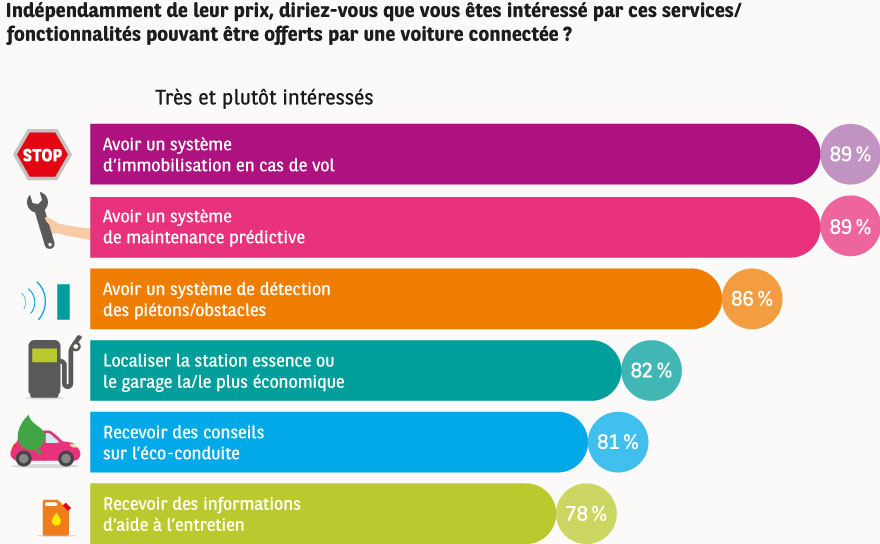

Les priorités : sécurité et économie

Pour trouver son public, le véhicule connecté devra en premier lieu garantir la sécurité des personnes et des véhicules. La réalisation d’économies financières ainsi que l’optimisation des temps de trajet sont aussi des attentes fortes.

Les automobilistes plébiscitent en priorité les systèmes d’immobilisation du véhicule en cas de vol (89 %). Compte tenu de la délinquance importante liée au véhicule dans leur pays, Mexicains et Brésiliens sont particulièrement intéressés par ces services (respectivement à 96 % et 95 %). Les systèmes de détection des piétons/obstacles sur la route suscitent également une attente forte (86 %), notamment dans les pays émergents où les taux de mortalité restent élevés. Les fonctions de maintenance prédictive, qui consistent à alerter le conducteur en cas de panne ou de problème imminents, trouvent aussi leur public parmi les automobilistes (89 %), et plus particulièrement en Chine, au Brésil et en Afrique du Sud (95 %), mais aussi aux États-Unis.

La voiture connectée devra également intégrer des systèmes d’optimisation du budget comme la localisation de stations essence ou de garage économiques, ou encore des modules d’éco-conduite prodiguant des conseils sur la conduite à adopter pour réduire la consommation de carburant.

D’autres systèmes, relatifs au divertissement ou destinés à faciliter les déplacements, sont plébiscités par les automobilistes, comme l’accès à des informations sur la localisation de commerces à proximité (73 %, n°7) ou la possibilité de localiser, réserver et payer une place de parking (71 %, n°8).

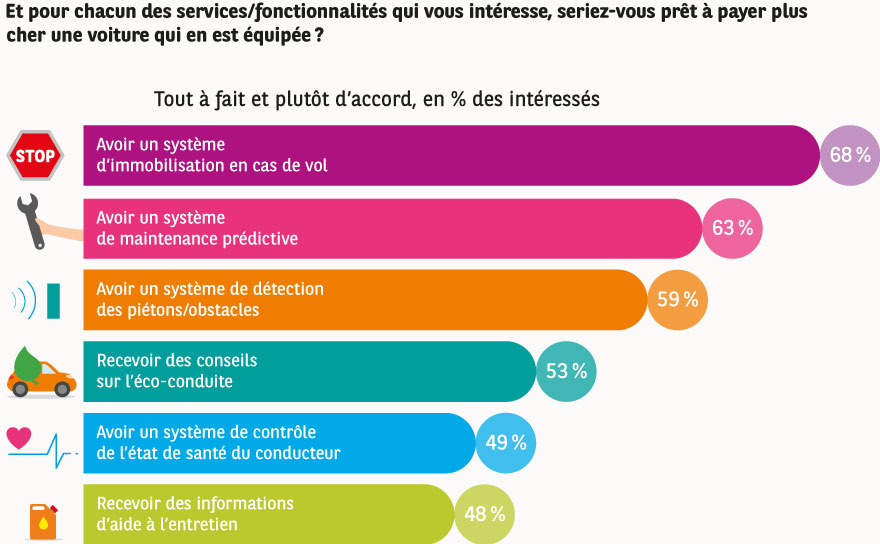

Investir pour sa sécurité et optimiser ses coûts

Les automobilistes sont nombreux à envisager payer plus cher pour bénéficier de fonctionnalités connectées remplissant les critères de sécurité et d’optimisation de leur budget.

Ce sont plutôt les consommateurs des pays émergents qui se montrent les plus disposés à payer : plus de la moitié des automobilistes intéressés sont prêts à investir pour recevoir des informations sur la localisation de commerces, utiliser Internet ou recevoir des messages, tandis qu’ils représentent moins d’un tiers dans les pays occidentaux.

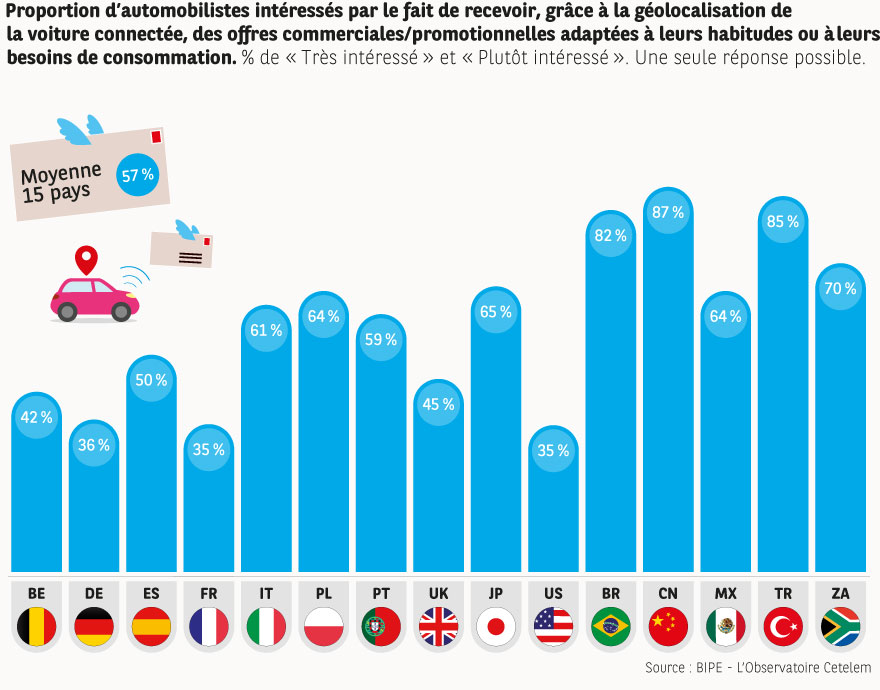

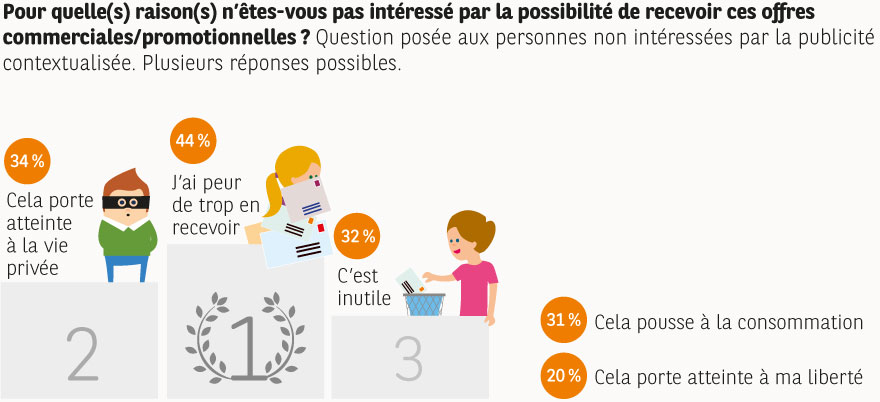

La publicité contextualisée, à consommer avec modération !

La géolocalisation de la voiture connectée permettra au consommateur de recevoir des offres commerciales ou promotionnelles adaptées à ses habitudes ou besoins de consommation. Et cette possibilité ravit 57 % des automobilistes en moyenne.

Si les Chinois se montrent les plus demandeurs d’offres commerciales personnalisées (87 %), en revanche Français (35 %), Allemands (36 %) et Américains (35 %) sont beaucoup plus réservés.

Pour les 43 % d’automobilistes qui déclarent ne pas être intéressés, la crainte provient avant tout de voir l’automobile se transformer en nouveau media publicitaire. Les automobilistes redoutent en effet que cette publicité personnalisée ne devienne trop invasive (44 %), et estiment même à 34 % que cela porte atteinte à leur vie privée.

Un levier de reconquête du consommateur

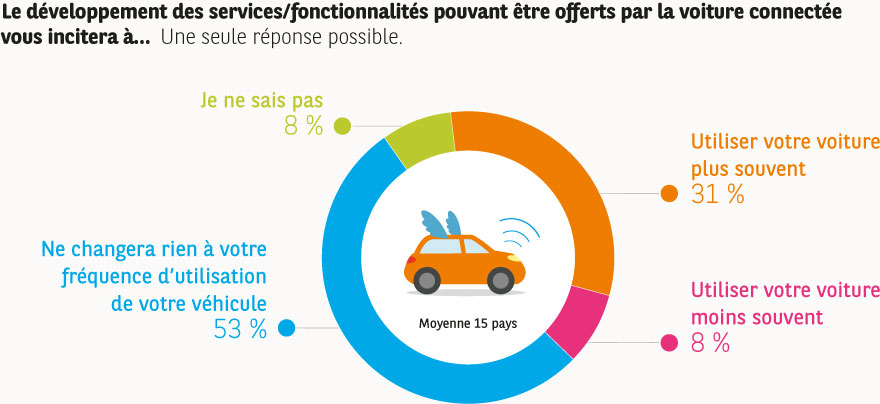

Au bilan, si pour 53 % des automobilistes interrogés, le véhicule connecté ne changera rien à leur fréquence d’utilisation du véhicule, 31 % estiment que les bénéfices apportés par les fonctionnalités connectées les inciteront à choisir plus souvent la voiture pour se déplacer, contre seulement 8 % d’intentions d’usage moins intense. En améliorant l’expérience de conduite et le temps passé en voiture, l’automobile connectée pourrait ainsi constituer un levier de (re)-conquête du consommateur.

Au bilan, l’arrivée du véhicule connecté et de sa version la plus aboutie qu’est le véhicule autonome pourraient bien marquer le renouveau du produit et du commerce automobile, tant les consommateurs les plébiscitent. Confort, gain de temps, sécurité… : des bénéfices attendus et reconnus par la majorité, qui se montre prête à payer pour en profiter. En rendant la mobilité urbaine davantage automobile, la voiture autonome représente bel et bien un levier de croissance pour les marchés de la vente et de l’après-vente.